Medicare Part D Enrollment Periods

Table of Contents

Medicare Part D provides prescription drug coverage for people enrolled in Original Medicare or Medicare Advantage plans that don't include drug coverage. Knowing when you can enroll — and what happens if you miss your window — is essential for avoiding gaps in coverage and costly penalties.

There are several distinct enrollment periods for Medicare Part D, each with its own rules and timelines. Here's what you need to know about each one.

"There are 4 key times that standalone Part D plans can be sold: the Initial Enrollment Period when a person is first enrolling into Medicare, the Annual Enrollment Period each year between October 15 and December 7, Special Enrollment Periods triggered most frequently by life events such as loss of creditable coverage or moving service areas, and the Medicare Advantage Open Enrollment Period from January 1 to March 31, but only if a Medicare member is changing from a Medicare Advantage plan back to traditional Medicare," says Tim Newsome, a licensed Medicare agent in Tennessee.

Initial Enrollment Period (IEP)

Your Initial Enrollment Period is a 7-month window that surrounds the month you first become eligible for Medicare. For most people, this is when they turn 65. The IEP includes:

- 3 months before your 65th birthday month

- Your birthday month itself

- 3 months after your birthday month

If you qualify for Medicare before 65 because of a disability, you get the same 7-month IEP built around your 25th month of Social Security disability benefits, not your birthday.

This is your first opportunity to enroll in a Medicare Part D plan. If you have creditable drug coverage through an employer, union, or other source, you may choose to delay enrollment without facing a penalty. However, if you go 63 or more consecutive days without creditable coverage and don't enroll during your IEP, you'll likely face a late enrollment penalty.

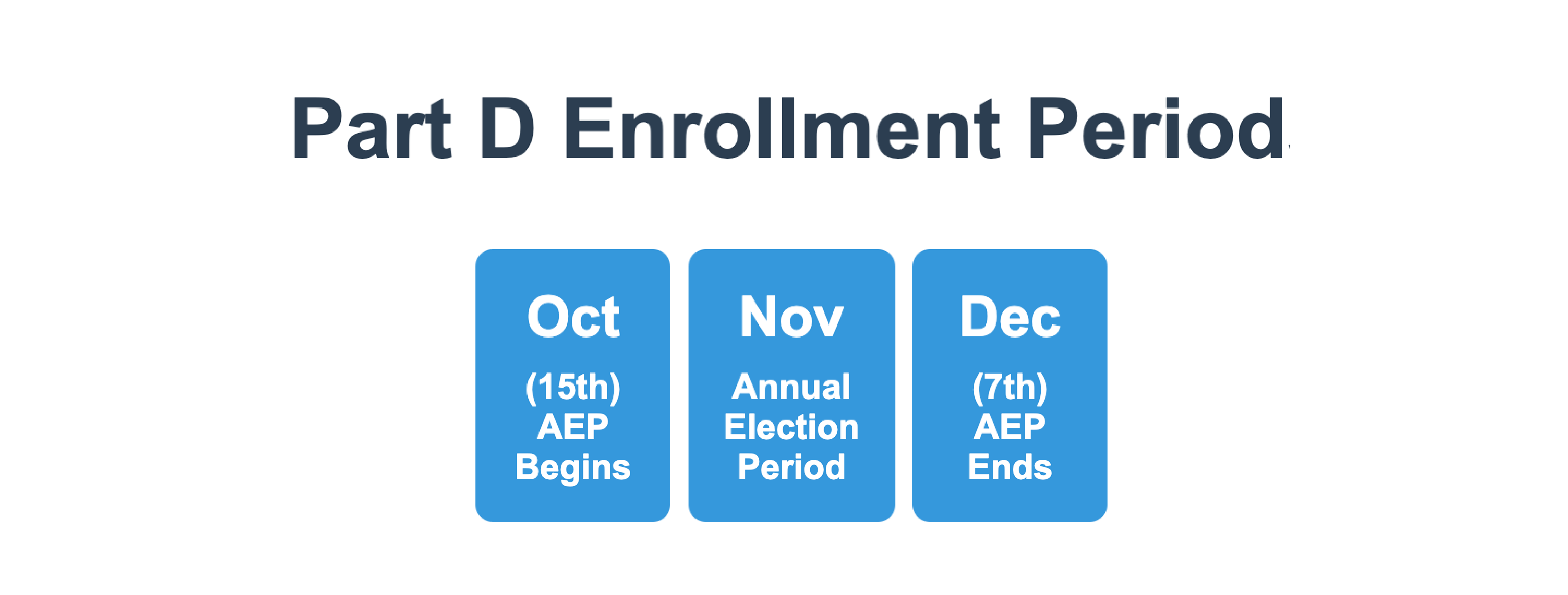

Annual Enrollment Period (AEP)

The Annual Enrollment Period — also called Open Enrollment — runs from October 15 through December 7 each year. Changes made during AEP take effect on January 1 of the following year.

During AEP, you can:

- Enroll in a Medicare Part D plan for the first time

- Switch from one Part D plan to another

- Drop your Part D plan (though this may trigger a penalty if you lose creditable coverage)

- Switch between Original Medicare and Medicare Advantage

This is the most common time people review their drug coverage. Since plan formularies, premiums, and copays can change year to year, it's important to review your Part D plan every fall — even if you're happy with your current coverage.

The reason annual review matters has gotten sharper in recent years. "It is important that you shop your Part D prescription coverage every year. In 2024 all the Part D carriers revised formularies because Congress mandated that in 2025 seniors would not have to pay more than $2,000 per year for prescription drugs. For this reason, many of the prescription plan revisions excluded some of the higher cost medications in their formularies," says Mike Sosso, a licensed Medicare agent in Texas. "If you are in a situation where your plan has excluded a medication you are taking, contact Medicare and your drug plan to ask for an exception."

That $2,000 annual out-of-pocket cap took effect January 1, 2025 and remains in place today, so the formulary shakeups Sosso describes are still playing out each fall. If a medication you rely on drops off your plan's formulary, don't wait to raise it during AEP.

Medicare Advantage Open Enrollment Period (MA OEP)

The MA OEP runs from January 1 through March 31 each year. This period is specifically for people who are already enrolled in a Medicare Advantage plan. During the MA OEP, you can:

- Switch from one Medicare Advantage plan to another

- Drop your Medicare Advantage plan and return to Original Medicare (and enroll in a standalone Part D plan at the same time)

You cannot use the MA OEP to switch from Original Medicare into a Medicare Advantage plan — that can only be done during AEP or a qualifying Special Enrollment Period.

One nuance trips up a lot of people during this window. "The Open Enrollment Period does not apply to those who want to change just their Part D RX plan," says Patricia Stiffler, a licensed Medicare agent in California. In other words, if you're on Original Medicare with a standalone Part D plan and you want to swap that Part D plan in February, you generally can't — you'll need to wait for AEP or qualify for a SEP.

Special Enrollment Periods (SEPs)

Special Enrollment Periods allow you to make changes to your Part D coverage outside of the standard enrollment windows. Qualifying life events that may trigger a SEP include:

- Losing employer or union drug coverage — you typically get a 2-month SEP

- Moving to a new service area where your current plan isn't available

- Qualifying for Extra Help (Low-Income Subsidy) — this gives you a SEP to change plans once per quarter

- Leaving a 5-star rated plan — you can switch once per year to any plan in your area

- Living in a nursing home or long-term care facility

- Losing Medicaid eligibility

If you experience one of these events, contact Medicare or a local insurance agent to confirm your SEP eligibility and enrollment deadline.

The moving SEP in particular has a tight clock. "As a rule, a person has three months to enroll in a new Medicare Advantage or Part D prescription drug plan that is available in the new location under the moving election SEP," says Louis Diez, a licensed Medicare agent in New York. "If a person misses the SEP window, they may have to wait until the next Annual Enrollment Period to make changes, which could leave that person without certain coverage for a period of time."

Medicare's official rule is a bit tighter for most people. If you tell your plan before you move, the window starts the month before your move and lasts 2 months after. If you tell them after you move, it starts the month you notify them plus 2 more months. Either way, don't wait — confirm your specific deadline with your plan or Medicare so you don't lose the SEP entirely.

The Part D Late Enrollment Penalty

If you go 63 or more consecutive days without Medicare Part D or other creditable prescription drug coverage, you may owe a late enrollment penalty when you eventually sign up. This penalty is calculated as follows:

- 1% of the national base beneficiary premium multiplied by the number of full months you went without creditable coverage

- The penalty is added to your monthly Part D premium and typically lasts for as long as you have a Part D plan

Example: If you went without creditable coverage for 14 months and the national base beneficiary premium is around $36.78 (CMS updates this figure each year, so check Medicare.gov for the current amount), your monthly penalty would be roughly $5.15 (14 × 1% × $36.78) — added on top of your regular plan premium every month.

The best way to avoid this penalty is to enroll in Part D during your IEP or maintain creditable drug coverage without any gaps longer than 63 days.

If you're already past your enrollment window and a penalty is on the table, enrolling now still helps. "You can sign up for a Medicare drug plan now, so you are protected going forward. You may have a penalty, but enrolling now stops the penalty amount from growing," says Marie Smith, a licensed Medicare agent in Alabama. "I also recommend applying for LIS, or Extra Help, the Low Income Subsidy. If you qualify, it may remove penalties and allow you to enroll in a Medicare Advantage plan sooner."

How to Enroll in a Part D Plan

When you're ready to enroll in or switch your Part D plan, you have several options:

- Medicare.gov Plan Finder — compare plans based on your specific medications, preferred pharmacy, and budget

- Call 1-800-MEDICARE (1-800-633-4227) for assistance over the phone

- Work with a licensed Medicare agent — an experienced agent can help you compare plans, check what your medications will cost under each option, and handle the enrollment paperwork

Before enrolling, make a complete list of your current prescriptions, including dosages. Check each plan's formulary to confirm your drugs are covered, and pay attention to the plan's tier structure, deductible, and copay or coinsurance amounts at your preferred pharmacy.

Tips for Choosing the Right Part D Plan

- Review your plan every year. Formularies, premiums, and pharmacy networks can change annually. What worked last year may not be the best value this year.

- Know how the coverage gap works today. The $2,000 annual out-of-pocket cap that took effect in 2025 essentially eliminates the old "donut hole" — once your yearly Part D out-of-pocket spending hits $2,000, covered drugs cost you nothing more for the rest of the year.

- Consider total cost, not just premiums. A plan with a low monthly premium may have higher copays or a larger deductible — compare total out-of-pocket costs based on the drugs you actually take.

- Verify your pharmacy is in-network. Using an out-of-network pharmacy can significantly increase your costs.

- Ask about Extra Help. If you have limited income and resources, you may qualify for the Low-Income Subsidy program that can dramatically reduce your Part D costs.

")