How to Apply for Medicare

Table of Contents

Applying for Medicare doesn't have to be complicated, but missing a deadline or skipping a step can lead to costly penalties and gaps in coverage. Whether you're approaching 65 or qualifying through a disability, this guide walks you through exactly how to apply for Medicare -- who's eligible, when to enroll, what documents you need, and how to submit your application.

Who Is Eligible for Medicare?

Most people become eligible for Medicare when they turn 65, provided they are a U.S. citizen or permanent legal resident who has lived in the country for at least five continuous years. You don't need to be retired or receiving Social Security benefits to qualify.

If you're under 65, you may still qualify for Medicare if you:

- Have received Social Security Disability Insurance (SSDI) benefits for 24 months

- Have been diagnosed with End-Stage Renal Disease (ESRD)

- Have been diagnosed with Amyotrophic Lateral Sclerosis (ALS / Lou Gehrig's disease) -- coverage begins the month your SSDI benefits start

When Can You Apply? (Enrollment Periods)

Medicare has specific enrollment windows. Applying at the right time is critical to avoiding late enrollment penalties and coverage gaps.

Initial Enrollment Period (IEP)

Your IEP is a 7-month window surrounding your 65th birthday: it starts 3 months before your birthday month, includes your birthday month, and extends 3 months after. This is the primary window for most people to enroll in Medicare.

Most agents recommend not waiting until the last minute. "It is recommended to apply three months before your birthday month to ensure coverage starts on time and avoid gaps," says Marcie Barnes, a licensed Medicare agent in Texas. "If you are already receiving Social Security or Railroad Retirement Board benefits at least four months before you turn 65, you will be automatically enrolled in both Part A and Part B."

General Enrollment Period (GEP)

If you missed your IEP, you can sign up during the General Enrollment Period, which runs from January 1 through March 31 each year. As of January 1, 2023, coverage begins the month after you enroll (the old "July 1" rule no longer applies). Keep in mind that late enrollment may result in a permanent premium surcharge on Part B.

Special Enrollment Period (SEP)

A Special Enrollment Period allows you to enroll outside the standard windows if you experience a qualifying life event -- most commonly, losing employer-sponsored health coverage. If you or your spouse had group health insurance through an employer, you typically get an 8-month SEP after that coverage ends.

The employer size matters here, though. "You will not have to pay a penalty if you are covered by your spouse's employer's group health plan, provided it has 20 or more employees. You can delay Part B enrollment until your spouse retires without a penalty, and will have an 8-month Special Enrollment Period to sign up once that coverage ends," says Ken Banks, a licensed Medicare agent in Georgia. "Verify the employer size first -- if it has fewer than 20 employees, you may face a late enrollment penalty."

Note that Part D has its own late-enrollment penalty (roughly 1% of the national base beneficiary premium for every month you go without creditable drug coverage), and its SEP is generally only 2 months long after losing creditable coverage. If you plan to add a Medigap policy, your best window to buy one is the 6-month Medigap Open Enrollment Period that starts the month you're 65 or older and enrolled in Part B -- during that window, insurers can't deny you coverage or charge more because of pre-existing conditions.

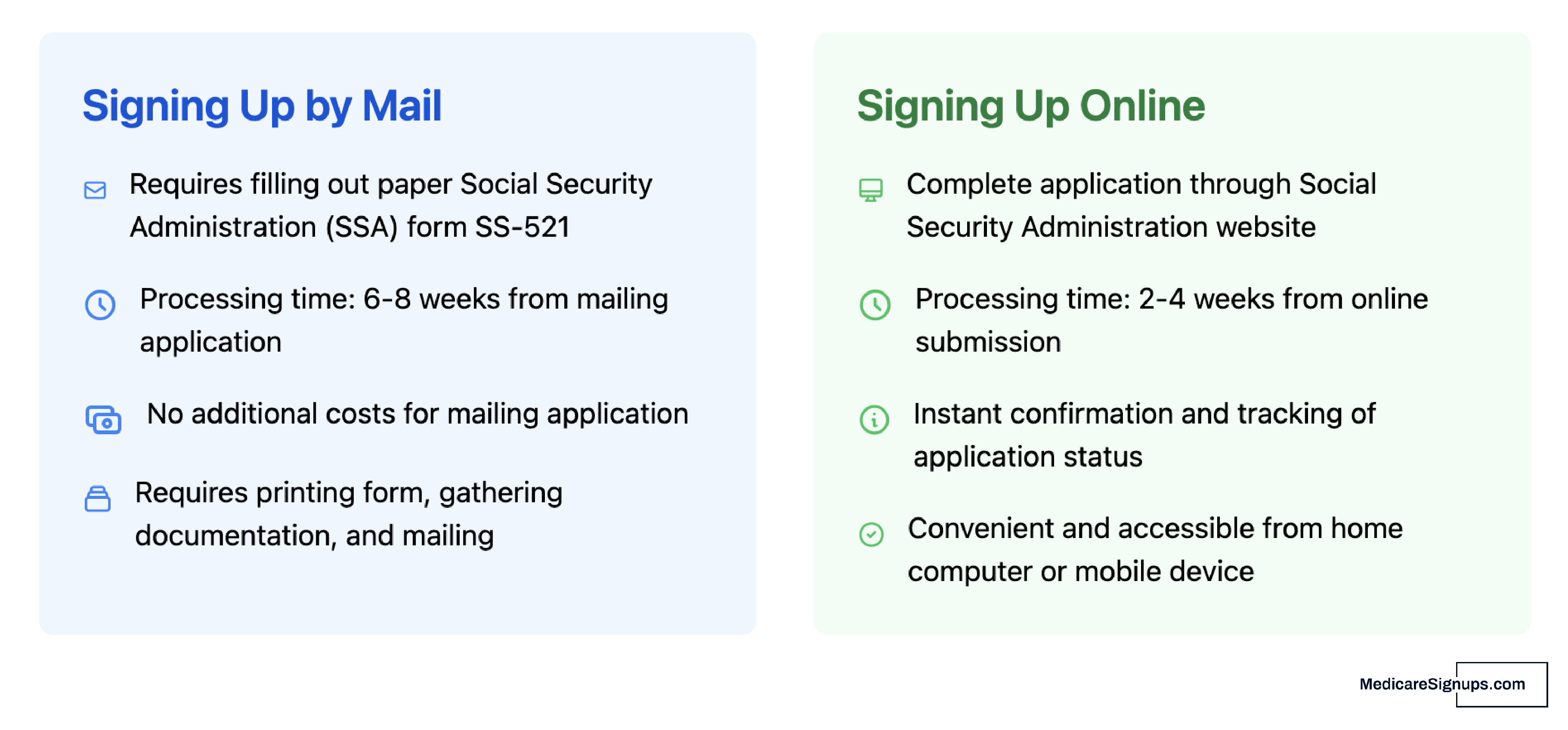

How to Apply for Medicare Online

The fastest way to apply for Medicare is online through the Social Security Administration. Here's the step-by-step process:

According to Julia Alves, a licensed Medicare agent in Florida, the timing matters as much as the method. "We are three months before your 65th birthday, which means the process to enroll and apply for Medicare starts now. You can visit your nearest Social Security office in person, call the Social Security office, or apply online at ssa.gov. This process can take a few weeks, so it is best to do this as soon as possible."

- Create a my Social Security account at ssa.gov/myaccount if you don't already have one

- Log in and select the option to apply for Medicare

- Complete the application -- you'll provide personal details, employment history, and insurance information

- Review and submit -- double-check all information before finalizing

- Save your confirmation number for your records

The online application typically takes 10-15 minutes if you have your documents ready. You can also save your progress and return later.

How to Apply at a Social Security Office

If you prefer to apply in person, you can visit your local Social Security office. However, be prepared for long wait times if you walk in without an appointment. To schedule an appointment, call 1-800-772-1213 (TTY: 1-800-325-0778).

You can also apply by phone by calling the same number. Phone applications are a good middle ground if you want personal assistance but can't easily get to an office.

What Documents Do You Need?

Gather these documents before you start your application to avoid delays:

- Social Security number

- Birth certificate or proof of U.S. citizenship/legal residency

- W-2 forms or self-employment tax returns from the past year

- Current employer information (if you or your spouse are still working)

- Health insurance details -- including any employer or union group coverage

- Military discharge papers (DD-214) if you served in the military

- Bank account information for direct deposit of any benefits

You may not need every document on this list -- it depends on your situation. The Social Security Administration will let you know if additional documentation is required.

The 6 Key Steps at a Glance:

- Check your eligibility -- age 65+, U.S. citizen or resident for 5+ years, or under 65 with a qualifying disability.

- Know your enrollment period -- IEP (7 months around 65), GEP (Jan 1 - Mar 31), or SEP (after losing job coverage).

- Gather your documents -- SSN, birth certificate, W-2 forms, employer info, insurance details.

- Choose how to apply -- online at ssa.gov (fastest, ~15 min), by phone, or at a local Social Security office.

- Submit and confirm -- review carefully, submit, and save your confirmation number.

- Receive your Medicare card -- SSA reviews your application and mails your card with coverage details.

Medicare, Social Security, and Railroad Retirement

Many people don't realize that you sign up for Original Medicare Parts A and B through the Social Security Administration -- not through Medicare directly. Here's how the connection works:

- Already receiving Social Security benefits? You'll be enrolled in Medicare Parts A and B automatically when you turn 65. Your Medicare card will arrive in the mail about 3 months before your 65th birthday.

- Deferred Social Security past 65? You'll need to proactively sign up for Medicare yourself. You're first eligible 3 months before you turn 65.

- Applying for Social Security or Railroad Retirement benefits? That application also serves as your Medicare application. Once approved, you'll automatically get Part A (premium-free if you or your spouse paid Medicare taxes for 40+ quarters).

If you're getting benefits from Social Security (or the Railroad Retirement Board) at least 4 months before you turn 65, you'll automatically get Part A and be signed up for Part B. Because Part B carries a monthly premium, you can choose whether to keep it or decline it.

You sign up through Social Security because they verify whether you (or a qualifying spouse) paid Medicare taxes long enough to receive Part A without a premium. They also process Part B enrollment requests.

One of the most common points of confusion involves delaying Social Security benefits. "Delaying Social Security until age 70 does not delay your Medicare enrollment, and this is an important distinction that often surprises people," says Sherri Beach, a licensed Medicare agent in Colorado. "Your Medicare eligibility is based on age, not when you begin collecting Social Security benefits. If you delay enrollment without other qualifying coverage, you could face late enrollment penalties and gaps in coverage."

If you or your spouse worked for a railroad, contact the Railroad Retirement Board at 1-877-772-5772 instead of Social Security.

What Happens After You Apply?

Once you've submitted your application, here's what to expect:

- Processing time: SSA typically processes applications in 2-4 weeks, though it can run longer during busy periods. Online applications tend to be faster than mailed or in-person filings.

- Medicare card: If approved, you'll receive a red, white, and blue Medicare card in the mail. It will show your Medicare number, the date your Part A and/or Part B coverage starts, and other details.

- Welcome packet: Along with your card, you'll receive the Medicare & You handbook with detailed information about your coverage options.

- Next steps: Once enrolled in Original Medicare, you can decide whether to add a Medicare Supplement plan, a Medicare Advantage plan, or a Part D prescription drug plan.

If your application is denied, Social Security will send a letter explaining the reason and your options for appeal.

Common Mistakes to Avoid

Don't let a simple mistake delay your coverage or cost you money. Here are the most frequent pitfalls:

- Missing your Initial Enrollment Period -- this can trigger permanent late enrollment penalties on your Part B premium

- Assuming enrollment is automatic -- it's only automatic if you're already receiving Social Security benefits

- Not understanding employer coverage rules -- if you're still working at 65, you may be able to delay Medicare, but the rules are specific

- Confusing Medicare Parts -- signing up for Parts A and B is just the beginning; you'll still need to choose additional coverage

If you do miss your window, the late enrollment penalty can be steeper than many people expect. "For Part B, there's a General Enrollment Period from January 1st to March 31st each year. If you sign up during GEP, you'll pay a 10% monthly penalty per year you missed," says Rich Baker, a licensed Medicare agent in Colorado. "It's cumulative, so if you waited an additional year, you'd pay 20%. And it's permanent -- you pay that penalty as long as you have Part B coverage. However, if you had employer coverage or spousal coverage that can be considered creditable, you have a different situation. VA coverage, COBRA, and ACA coverage are not creditable, so it pays to verify with an agent before assuming you're protected."

For a deeper dive, read about common Medicare mistakes first-time enrollees make so you can sidestep the most expensive errors.

If you have questions during the application process, contact Social Security at 1-800-772-1213 (TTY: 1-800-325-0778). Representatives are available Monday through Friday, 8:00 a.m. to 7:00 p.m. For questions about Medicare coverage itself (not enrollment), call Medicare directly at 1-800-MEDICARE (1-800-633-4227), available 24/7.

Medicare rules, deadlines, and premiums can change year to year. Always verify current information at Medicare.gov or with a licensed agent before making enrollment decisions.

Matt Feret

Author, Prepare for Medicare - The Insider’s Guide

https://prepareformedicare.com

Matt Feret is the author of the Prepare for Social Security - The Insider’s Guide and the Prepare for Medicare - The Insider’s Guide book series and launched PrepareforSocialSecurity.com to help people get objective answers to questions about Social Security and Medicare. Matt is also the host of The Matt Feret Show. He has held leadership roles at numerous Fortune 500 Medicare health insurers in sales, marketing, operations, product development, and strategy for over two decades.