Medicare Part C

Table of Contents

Medicare Part C, commonly known as Medicare Advantage, is a bundled alternative to Original Medicare offered by private insurance companies approved by Medicare. Instead of getting separate Part A and Part B coverage through the federal government, a Medicare Advantage plan delivers all of your Medicare benefits through a single plan — often with additional perks like dental, vision, and prescription drug coverage (Part D).

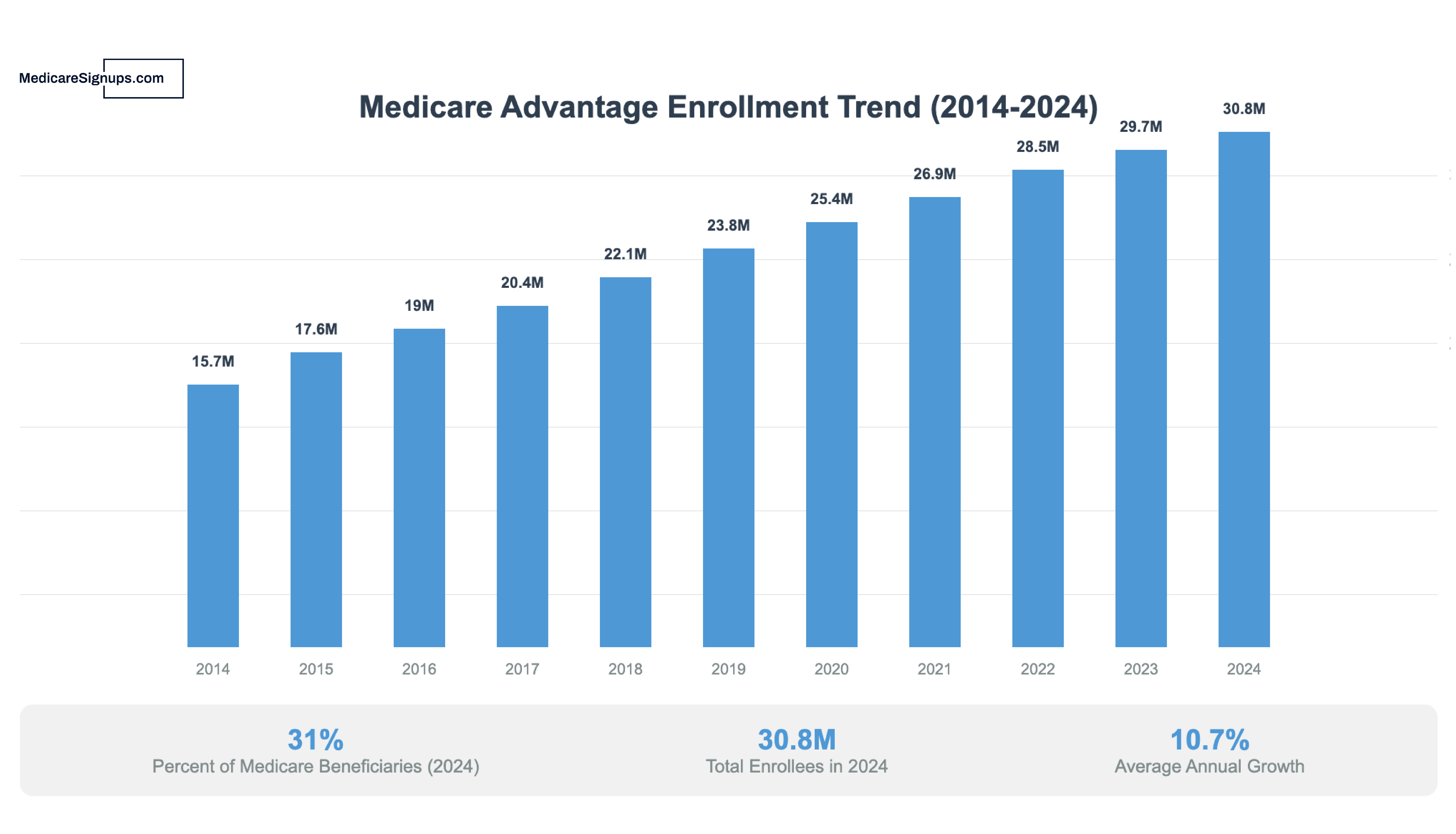

With more than half of all Medicare beneficiaries now enrolled in a Part C plan, Medicare Advantage has become the most popular way to receive Medicare benefits in the United States (source: KFF Medicare Advantage 2026 Enrollment Update).

How Does Medicare Part C Work?

Medicare Advantage plans are offered by private insurance companies that contract with Medicare. These companies must cover everything that Original Medicare (Parts A and B) covers, but they can structure costs, networks, and additional benefits differently. When you enroll in a Part C plan, Medicare pays the insurer a fixed amount per month on your behalf, and the insurer manages your care.

Most Medicare Advantage plans use provider networks — such as HMO or PPO structures — to coordinate care and manage costs. HMO plans typically require you to use in-network providers and get referrals for specialists, while PPO plans offer more flexibility to see out-of-network doctors at a higher cost. Understanding how these networks work is key to choosing the right plan.

“Medicare Advantage plans have evolved over the last several years. Most of them are now PPOs, which means you can go to doctors not in the network. They've added benefits that Medicare does not cover like dental coverage, eyeglass coverage, over-the-counter items, even hearing aids”

— Walt Smith, a licensed Medicare agent in New Jersey

That shift toward PPO structures and richer extras is a big part of why enrollment in Part C has climbed so fast.

Key Benefits of Medicare Advantage

✅ Lower Costs & Budget-Friendly – Many plans offer $0 monthly premiums and set an annual out-of-pocket maximum, protecting you from high medical bills (Original Medicare has no limit).

✅ Extra Benefits at No Extra Cost – Enjoy perks like gym memberships, transportation, meal delivery, hearing aid coverage, and over-the-counter allowances to support your health.

✅ Coordinated & Simplified Care – Medicare Advantage plans use managed care networks, making it easier to coordinate treatments and reduce unnecessary expenses.

✅ One Plan, One Provider – Instead of enrolling in separate Medicare Supplement (Medigap) and Part D plans, Medicare Advantage bundles everything into one simple plan.

That $0 premium headline does come with some fine print, though.

“Most Medicare Advantage are $0 premium plans that have co-pays, co-insurances and most importantly, a maximum out-of-pocket in-network. These plans are frequently called Pay As You Go plans. You may not spend anything or you may spend the max out of pocket. No one knows what health issues will arise in the future”

— Jim Schueth, a licensed Medicare agent in Nebraska

The point isn't that the plans aren't a good deal — many are — it's that you should budget for the possibility of hitting that maximum in a bad health year.

The extras can also be more substantial than people expect.

“The right healthcare company will have your physicians and hospitals in their network, reasonable copays, extra benefits you want such as dental, vision, hearing, over-the-counter benefits, gym memberships and a rewards card for keeping up with your health appointments”

— Rene Casanova, a licensed Medicare agent in Texas

Check out this graph showing the dramatic increase in Medicare Advantage enrollment in the last 10 years.

Medicare Advantage Eligibility

To enroll in a Medicare Advantage plan, you must meet a few basic requirements:

- You must be enrolled in both Medicare Part A and Part B

- You must live in the plan's service area

- You cannot be enrolled in hospice care at the time you sign up (hospice benefits stay with Original Medicare)

In the past, people with End-Stage Renal Disease (ESRD) were generally locked out of Medicare Advantage. That changed with the 21st Century Cures Act: since January 2021, anyone with ESRD is eligible to enroll in an MA plan during their normal election period, just like any other beneficiary.

Most people first become eligible when they turn 65 and enroll in Medicare. If you qualify for Medicare through a disability, you can also join a Medicare Advantage plan. For a broader look at who qualifies for Medicare, see our guide on Medicare eligibility.

Types of Medicare Advantage Plans

Not all Part C plans work the same way. The main types include:

- HMO (Health Maintenance Organization) – Requires in-network providers and referrals for specialists. Typically the lowest premiums.

- PPO (Preferred Provider Organization) – Offers more flexibility with out-of-network care at a higher cost. Great for people who travel or see multiple specialists. Learn more about Medicare PPO plans.

- PFFS (Private Fee-for-Service) – Determines how much providers are paid and how much you pay when you receive care. Less common than HMO or PPO.

- SNP (Special Needs Plans) – Designed for people with specific diseases, certain income levels, or those who are dually eligible for Medicare and Medicaid.

The insurance companies offering these plans will vary by county, but the big national carriers you'll see quoted most often are UnitedHealthcare, Humana, Aetna, Cigna, and the regional Blue Cross Blue Shield affiliate for your state. Regional and provider-sponsored plans (such as Kaiser Permanente in certain markets) round out the field. Availability, networks, and extra benefits differ from one carrier to the next, so it's worth pulling quotes from more than one before you commit.

Special Needs Plans actually break down further depending on what makes someone eligible.

“There are several types of Medicare Advantage plans including HMOs, PPOs, PFFSs and MSA plans. There are plans called MA only (those without a Part D) and those called MAPD (which include Part D). There are also plans tailored to specific populations and these are referred to as Special Needs Plans — they include CSNP for those with chronic conditions, DSNP for those who have both Medicare and Medicaid, and ISNP for institutionalized individuals”

— Jane Ahrens, a licensed Medicare agent in New York

If you have a qualifying chronic condition or are dual-eligible, asking about an SNP specifically can open up plans built for your situation.

Each plan type has trade-offs between cost, flexibility, and provider choice. Use our step-by-step plan comparison checklist to weigh the differences.

Medicare Advantage Enrollment Periods

You can't enroll in or switch Medicare Advantage plans at just any time. There are specific windows:

- Initial Enrollment Period (IEP) – The 7-month window around your 65th birthday (3 months before, your birthday month, and 3 months after).

- Annual Enrollment Period (AEP) – October 15 through December 7 each year. This is when most people make changes to their Medicare coverage.

- Open Enrollment Period (OEP) – January 1 through March 31. If you're already in a Medicare Advantage plan, you can switch to a different plan or return to Original Medicare.

- Special Enrollment Period (SEP) – Triggered by qualifying life events like moving out of your plan's service area, losing employer coverage, or becoming eligible for Medicaid. SEPs let you enroll or switch outside the standard windows.

Missing these windows can limit your options. Delaying Part D drug coverage in particular can trigger late enrollment penalties that get added to your premium for life. For a detailed breakdown, see our full guide on Medicare Advantage enrollment periods.

Medicare Part C vs Original Medicare

Choosing between Medicare Advantage and Original Medicare is one of the biggest decisions new beneficiaries face. Here's a quick comparison:

- Cost structure – Original Medicare has no out-of-pocket maximum, meaning your costs are theoretically unlimited. Medicare Advantage plans cap your annual spending.

- Provider flexibility – Original Medicare lets you see any doctor who accepts Medicare, anywhere in the country. Part C plans often restrict you to a network.

- Additional benefits – Part C plans frequently include dental, vision, hearing, and fitness benefits that Original Medicare does not cover.

- Supplemental coverage – With Original Medicare, you can purchase a Medigap policy to cover gaps. With Medicare Advantage, Medigap is generally not available.

| Feature | Original Medicare | Medicare Advantage (Part C) |

|---|---|---|

| Out-of-pocket max | None | Annual cap set by plan |

| Provider choice | Any provider that accepts Medicare, nationwide | Usually restricted to plan network |

| Extra benefits | Not included (dental, vision, hearing) | Often included |

| Prescription drugs | Requires separate Part D plan | Usually bundled (MAPD) |

| Medigap compatibility | Can add Medigap to fill cost gaps | Medigap generally not allowed |

What to Consider Before Choosing Part C

Medicare Advantage is a strong option for many beneficiaries, but it's not the right fit for everyone. Before enrolling, think about:

- Network restrictions – Will your current doctors and hospitals be in-network? Switching plans could mean switching providers.

- Travel – If you spend significant time outside your plan's service area, an HMO plan may not cover care away from home.

- Referral requirements – Some plans require referrals to see specialists, which can slow down access to care.

- Plan quality – Check Medicare Star Ratings to compare plan quality in your area before enrolling.

The network question is the one that trips up the most people.

“If you have a Medicare Advantage HMO, you are limited to the doctors in the medical group you choose, and you are limited in which medical groups work with which HMO. For Medicare Advantage PPO plans, the biggest disadvantage is the copays and higher out of network costs and maximum out of pocket”

— Helena Foutz, a licensed Medicare agent in California

Before you enroll, pull out your prescription list and your provider list and confirm both are covered — not assumed.

Hospital access is also worth checking carefully.

“That is a contractual issue between the hospital and the insurance carrier. If they're not taking a Medicare Advantage plan, they have their reasons for it. Typically if you stay with major brands you don't have that problem — it's when you get these small off-brand companies that are the ones that tend to make it harder to find in-network hospitals”

— Gary Henderson, a licensed Medicare agent in Texas

A plan with a flashy benefit package isn't worth much if the big hospital system in your area refuses to take it.

If you're looking for affordable, comprehensive Medicare coverage, Medicare Advantage could be the right choice. Plans vary by location, so compare options to find one that fits your healthcare needs.

Need help with Medicare? Find the best Medicare Advantage plan in your area and get coverage that works for you!